Qualified Small Business Stock Exemption

Section: 1202

It’s no secret that small businesses have long been the growth engine of the US economy. With that in mind, Congress has packed the tax code with lots of breaks for those investing in small companies. One of the best, but little known breaks became permanent with the passage of the Protecting Americans from Tax Hikes (PATH) Act on December 18, 2015. I am referring to qualified small business stock (QSBS), a big reason for venture capitalists, angel investors, and entrepreneurs to smile in 2016 and beyond.

What is a Qualified Small Business Stock Exemption?

QSBS is stock in a United States C corporation that had gross assets of $50 million or less at all times before and immediately after the issuance of the QSBS and has been actively engaged in a “qualified trade or business.” What constitutes a qualified trade or business is pretty broad, though it excludes certain service businesses (like law, healthcare, financial services and architecture), financial businesses (like banking and insurance), and other specified industries (farming, mining, hospitality and restaurants). While this list is not exhaustive, in our experience many early-stage investments in technology companies meet these requirements and thus stock in many startups can qualify as QSBS.

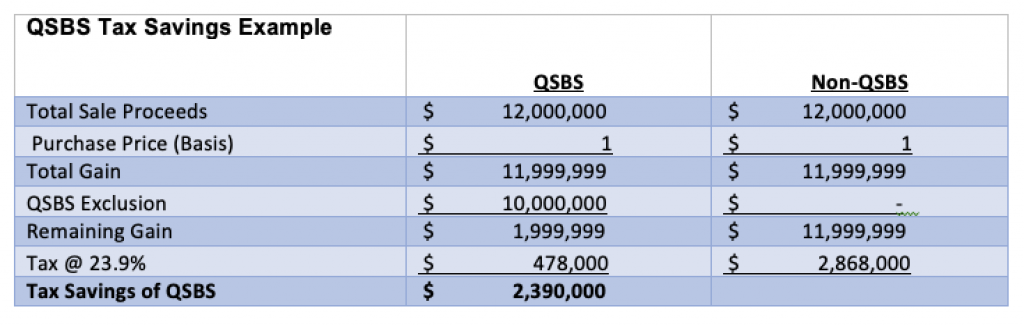

Example of Qualified Small Business Stock Exclusion

KEY TAKEAWAYS:

- Under Section 1202, capital gains from select small business stocks are excluded from federal tax.

- It provides an incentive for non-corporate taxpayers to invest in small businesses.

- Not all small business stocks qualify, however.

- The amount of gain excluded under Section 1202 is limited to a maximum of $10 million or 10 times the adjusted basis of the stock.

The The First Step

Requirements of Section 1202

Not all small business stocks are qualified for tax breaks under the IRC. The Code defines a small business stock as qualified if:

- It was issued by a domestic C-corporation other than a hotel, restaurant, financial institution, real estate company, farm, a mining company, or business relating to law, engineering, or architecture

- It was originally issued after August 10, 1993, in exchange for money, property not including stocks, or as compensation for a service rendered

- On the date of stock issue and immediately after, the issuing corporation had $50 million or less in assets

- The use of at least 80% of the corporation’s assets is for the active conduct of one or more qualified businesses

- The issuing corporation does not purchase any of the stock from the taxpayer during a four-year period beginning two years before the issue date

- The issuing corporation does not significantly redeem its stock within a two-year period beginning one year before the issue date. A significant stock redemption is redeeming an aggregate value of stocks that exceed 5% of the total value of the company’s stock

State taxes that conform to federal tax will also exclude capital gains of small business stock. Since not all states correlate with federal tax directives, taxpayers should seek guidance from their accountants on how their states treat realized profits from the sale of qualified small business stocks.